Why do you need a financial advisor for managing your funds?

Why do you need a financial advisor for managing your funds? In an era of one-click investment apps, the question has shifted from “How do I buy?” to “What should I buy and why?” While technology makes the markets accessible, it doesn’t provide the wisdom needed to navigate them. Managing wealth for milestones like a child’s overseas education or a peaceful retirement requires more than a digital interface it requires a Financial Architect. What Does a Financial Advisor Do? If you are wondering, “What does a financial advisor do exactly?”, the answer involves much more than picking “hot” stocks. A professional advisor serves as a strategist, a risk manager, and an emotional anchor. Their core responsibilities include: Customized Asset Allocation: Beyond just stocks, they balance your wealth across equity, debt, real estate, and alternative assets based on 2026 market dynamics. Tax Efficiency (Tax Alpha): Implementing strategies to ensure you legally keep a larger portion of your investment gains. Behavioral Coaching: Acting as an “Emotional Shield” to prevent you from making panic-driven sales during market dips or “FOMO” buys during hype cycles. Goal-Based Engineering: Calculating the exact math required to reach your future targets, adjusted for inflation. How to Choose a Financial Advisor Knowing how to choose a financial advisor is perhaps the most critical financial decision you will make. In 2026, look for these three pillars of excellence: Fiduciary Credentials: Ensure they are registered professionals. If you have ever researched how to become a financial advisor in India, you know it requires rigorous certifications (like NISM or CFP) and adherence to strict ethical codes. Fee Transparency: A professional advisor should be upfront about their compensation structure. There should be no “hidden costs” in the products they recommend. Proactive Communication: The markets move at lightning speed. You need an advisor who reaches out to you with updates, rather than one who only responds when you call. The “Human Touch” in a Digital World While AI-driven “robo-advisors” have grown, many high-net-worth investors still value a personal partnership. Searching for a “financial advisor near me” is often the first step toward finding a partner who understands your local economic context—whether it’s the nuances of local real estate or specific tax implications for your business. A local advisor provides face-to-face accountability that an algorithm simply cannot replicate. Why Strategic Fund Management Matters Managing funds in 2026 requires staying ahead of global trends (like AI-led market shifts) while maintaining a disciplined, long-term perspective. Professional management offers: Holistic Life Planning: An advisor doesn’t just manage your “bank balance”; they manage your life’s timeline, from your first SIP to your estate’s succession. Dynamic Rebalancing: Markets change. A professional ensures your portfolio is “pruned” and re-aligned with your risk profile at least twice a year. In a Nutshell A great financial advisor shouldn’t just tell you where to invest; they should explain why. If your investment strategy is so complex that it can’t be explained in simple terms, it might be built on the wrong foundation. Choosing to delegate market stress to a professional is often the first “investment” that pays real dividends. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Why do you need a financial advisor for managing your funds? Read More January 14, 2026 Behind the Scenes: How Fund Management Companies Maximize Returns Read More January 14, 2026 Why You Need a Financial Advisor to Secure Your Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

Why Do You Need an Insurance Advisor?

Why Do You Need an Insurance Advisor? In 2026, the insurance landscape has moved far beyond simple tax-saving tools. With complex medical tech, hyper-personalized motor plans, and new government initiatives like the Ayushman Vay Vandana scheme, the “Buy Now” button on a website can be deceptive. Many realize too late that the cheapest policy often comes with the most exclusions. As your insurance partner, we bridge the gap between holding a “policy document” and having “actual protection.” Here is why a professional advisor is your most valuable asset in 2026. 1. Navigating the 2026 “Complexity Gap” Modern policies are filled with nuanced clauses. In 2026, we see more “Managed Care” features, room rent rationalization, and AI-driven underwriting that can be difficult to decode. The Problem: An algorithm doesn’t know your family’s specific medical history or that your daily commute involves waterlogged streets. The Solution: An advisor acts as a Policy Translator. We decode terms like co-payments, domiciliary hospitalization, and “modern treatment” sub-limits into plain English, ensuring you aren’t hit with a surprise 30% out-of-pocket bill during a crisis. 2. Personalized Risk Mapping (Beyond the Algorithm) Online portals use generic data; a professional advisor uses context. Health: We ensure your plan includes the best local networks and specific coverage for “Daycare procedures” which are common in 2026. Motor: We advise on critical add-ons like Engine Protection or Return to Invoice—essentials that a generic online bot might deprioritize to show you a “lower” price. Life: We align your sum assured with the 2026 inflation rate, ensuring your family’s future isn’t undervalued by a plan made three years ago. 3. Your Advocate During the “Moment of Truth” The true test of insurance is the claim process. During an emergency, the last thing you want is to be on hold with a toll-free number. The Advisor Advantage: We act as your human liaison. From gathering documents to negotiating with the TPA (Third Party Administrator), we stand by you. Our goal is to ensure your claim is settled fairly and fast, leveraging professional relationships that an individual buyer simply doesn’t have. 4. Integration with Government Schemes With the 2026 expansion of the Ayushman Vay Vandana (offering free ₹5 lakh coverage for seniors aged 70+), many citizens now have dual coverage. The Strategy: A professional advisor helps you understand how to use these government benefits alongside your private insurance to reduce your private premiums (by using the govt scheme as a base) without losing high-end medical access. Comparison: Buying Online vs. Professional Advisor Feature Buying Online (Direct) Buying via Professional Advisor Selection Based on price/lowest premium Based on need/claim history Claim Support Self-service / Call center Personal advocate / End-to-end help Policy Audit None (Static) Regular reviews & updates Hidden Clauses Often missed in the fine print Explained and avoided Conclusion: More Than Just a Policy Insurance is a promise of a “future payment” in exchange for “current peace of mind.” To ensure that promise is kept, you need an expert who understands the system from the inside out. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Behind the Scenes: How Fund Management Companies Maximize Returns Read More January 14, 2026 Why You Need a Financial Advisor to Secure Your Read More January 14, 2026 The Role of Mutual Fund Distributors in Wealth Creation Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

Modern people’s guide to managing finances

Modern people’s guide to managing finances In 2026, the question is no longer just about “getting covered,” but about strategic medical planning. As medical inflation in Indian metros touches 14%, the way you structure your family’s health insurance can save you lakhs in premiums and out-of-pocket costs. At Welfin, we analyze your household’s unique health profile to decide whether you need an “Umbrella” (Family Floater) or “Shields” (Individual Plans). 1. The Foundation: What is Finance in Financial Management? To master your money, you must first understand the pillars. In 2026, finance is fundamentally the art of resource optimization. It involves three critical functions: Capital Acquisition: Identifying efficient sources of funds, whether through optimized salary structures, business revenue, or smart credit. Capital Allocation: Deciding where every rupee goes to generate the highest “inflation-adjusted” return. In the current landscape, this means balancing traditional assets with technology-led growth. Risk Mitigation: Using insurance and diversification as a structural “safety net” to ensure your progress isn’t wiped out by a single market dip or health emergency. 2. Personal Finance in the “Subscription Economy” Traditional budgeting is evolving. Managing personal finances in 2026 requires a tech-forward approach to combat “lifestyle creep” and the invisible drain of the subscription economy. The “Anti-Budget” Strategy: Instead of tracking every small purchase, focus on “Pay Yourself First.” Automate your SIPs and insurance premiums to leave your bank account the day your income arrives. What remains is yours to spend, guilt-free. Asset Allocation 2.0: With the 2026 inflation trends, a simple savings account is often a losing strategy. A modern portfolio typically follows a “Core and Satellite” model: 70% in stable, long-term diversified funds and 30% in high-growth tactical assets. Tax Alpha: Beyond the standard deductions, 2026 investors focus on tax-loss harvesting and capital gains optimization. With LTCG at 12.5% on gains above ₹1.25 lakh, timing your exits and reinvesting strategically can significantly increase your net take-home returns. 3. Business Finance for the New-Age Entrepreneur For the modern startup and SME community, financial management is the difference between scaling and failing. Cash Flow vs. Profit: A business can be profitable on paper but go bankrupt due to poor cash flow. Use digital forecasting tools to monitor your “Runway”—the number of months you can operate without new revenue. Separation of Funds: Never mix personal and business accounts. In 2026, automated cloud accounting makes this easier than ever, but the discipline must start with the founder. The “Peace Fund”: Aim for a business contingency buffer that covers at least 6 months of fixed overheads (rent, salaries, and cloud infrastructure costs) to navigate market volatility. 4. Modern Principles of Wealth Management True financial management is as much about mindset as it is about math: Audit Your Subscriptions: In the modern economy, “silent deductions” for unused apps or streaming services can drain thousands annually. Perform a quarterly “subscription audit.” Avoid Lifestyle Creep: As your income grows, try to keep your expenses steady. This “widening gap” is where true wealth is built. Data vs. Perspective: While apps provide data, an advisor provides perspective. Automated tools can show you what happened, but an expert explains why and what to do next. Summary Checklist for 2026 Area Strategy Goal Savings Automate at Source Eliminate manual discipline errors. Tax Capital Gains Optimization Use the ₹1.25L LTCG limit effectively. Spending Subscription Audit Stop “micro-leaks” in your budget. Risk 6-Month Emergency Fund Protect against career or market shocks. Conclusion Managing finances in 2026 is about being proactive, not reactive. By understanding the core of financial management and applying it to both your personal and professional life, you secure a future that is resilient to any economic storm. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Financial Planning process in 2026 Read More January 14, 2026 Why do you need a financial advisor for managing your funds? Read More January 14, 2026 Behind the Scenes: How Fund Management Companies Maximize Returns Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

Which health insurance is good for you Individual health insurance or a Family health Insurance plan

Which health insurance is good for you Individual health insurance or a Family health Insurance plan In 2026, the question is no longer just about “getting covered,” but about strategic medical planning. As medical inflation in Indian metros touches 14%, the way you structure your family’s health insurance can save you lakhs in premiums and out-of-pocket costs. 1. Understanding the Family Floater Plan A Family Floater is an “umbrella” policy where a single sum insured (e.g., ₹15 lakh) is shared by all covered members—usually you, your spouse, and up to four children. The Advantage: It is the most cost-effective way to cover a young, healthy family. Managing one policy is simpler, and the premium is significantly lower than buying four separate individual plans. The Risk: The sum insured “floats.” If one member uses ₹12 lakh for a major surgery, only ₹3 lakh remains for the other three members for the rest of the year. Best For: Young nuclear families (parents under 45) with no chronic illnesses. 2. When Individual Health Insurance is Wiser Protecting the Pool: If a family member has a chronic condition (like Diabetes or Hypertension), their frequent claims can exhaust a shared floater quickly. Giving them an individual plan “ring-fences” the rest of the family’s coverage. The “Eldest Member” Premium Trap: In a floater, the premium is calculated based on the oldest person. If you include a 65-year-old parent with a 30-year-old couple, the entire family’s premium is billed at senior-citizen rates. Best For: Seniors (60+), individuals with pre-existing diseases, or large multi-generational households. Individual vs. Family Floater: 2026 Comparison Matrix Feature Individual Health Plan Family Floater Plan Sum Insured Dedicated to one person only Shared across the entire family Premium Cost Higher (per person) Lower (bulk discount for families) No Claim Bonus Only the claimant’s bonus resets The entire family’s bonus may reset Ideal For High-risk individuals/Seniors Young, healthy nuclear families 3. The Welfin “Hybrid Strategy” for 2026 We often recommend a Hybrid Approach to balance cost and safety: For the Couple & Kids: Use a Family Floater (₹10L–₹15L). It’s affordable and sufficient for young members. For Parents (Seniors): Buy separate Senior Citizen Individual Plans. This prevents their age from inflating your premium and ensures they have a dedicated fund for age-related ailments. The “Super Top-Up” Hack: Instead of a ₹50 lakh base plan (which is expensive), buy a ₹5 lakh base plan and add a ₹45 lakh Super Top-Up. This provides high coverage for “black swan” events at a fraction of the cost. 4. Critical 2026 Features to Look For Regardless of the plan type, ensure your policy includes these “Safety Switches”: Unlimited Restoration: Automatically refills your sum insured if it gets used up mid-year. No Room Rent Caps: Essential for staying in private cabins at leading hospitals without paying a “pro-rata” penalty on the entire bill. Modern Treatment Cover: In 2026, ensure robotic surgeries and stem cell therapies are covered up to the full sum insured. In a Nutshell Choosing the right plan is about Risk Mapping. If your family is young and healthy, a Floater is a financial win. But if you have elders or specific health risks, Individual plans are the only way to ensure everyone is truly protected. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Which health insurance is good for you Individual health insurance or a Family health Insurance plan Read More January 14, 2026 Why choose zero dep Insurance for your new car Read More January 14, 2026 Precision Wealth: Why Portfolio Management Companies Are Essential Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

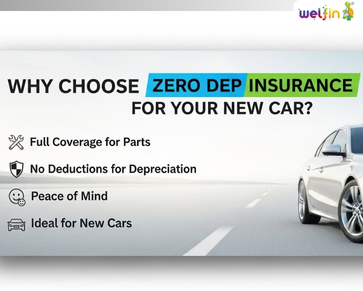

Why choose zero dep Insurance for your new car

Why choose zero dep Insurance for your new car Buying a new car is a landmark achievement. However, the moment you drive it out of the showroom, its value begins to drop due to a process called Depreciation. In 2026, where vehicle technology is more complex and repair costs are higher than ever, a standard comprehensive policy may leave you with a significant “out-of-pocket” bill after an accident. This is where Zero Depreciation (Zero Dep) insurance becomes an essential safety net. What is Zero Depreciation Insurance? Buying a new car is a landmark achievement. However, the moment you drive it out of the showroom, its value begins to drop due to a process called Depreciation. In 2026, where vehicle technology is more complex and repair costs are higher than ever, a standard comprehensive policy may leave you with a significant “out-of-pocket” bill after an accident. This is where Zero Depreciation (Zero Dep) insurance becomes an essential safety net. What is Zero Depreciation Insurance? Often called “Bumper-to-Bumper” insurance, Zero Dep is an optional add-on for your comprehensive car policy. In a standard policy, if you replace a damaged part, the insurer pays the “depreciated value” based on the part’s material and the car’s age. For example, plastic and rubber parts can see a 50% deduction. With a Zero Dep add-on, the insurer waives these deductions and pays the full cost of the parts (minus a small mandatory deductible). Why It Is Non-Negotiable for New Cars in 2026 Full Claim Payouts: Without this cover, you could end up paying for nearly half of the expensive parts (like fiber bumpers or LED headlights) out of your own pocket. High-Tech Parts Protection: Modern 2026 cars are packed with sensors and expensive electronics. Zero Dep ensures you aren’t financially burdened by the high cost of these “smart” components. Financial Predictability: It transforms an unpredictable repair bill into a fixed, manageable premium, providing peace of mind in heavy traffic. How to Check if You Have Zero Dep Policy Schedule: Look for the “Add-ons” or “Endorsements” section. It will be listed as “Nil Depreciation” or “Depreciation Reimbursement.” Premium Breakup: Check if an additional premium has been charged for this specific rider. Digital Verification: Log in to the mParivahan app or the VAHAN portal; your policy details will clearly show the “Bumper-to-Bumper” status Key Comparisons at a Glance Feature Standard Comprehensive Zero Dep Insurance Claim Settlement Based on depreciated value 100% of parts value Out-of-pocket Expense High (30% to 50% of parts) Minimal (only mandatory fees) Claim Limit Usually unlimited Often limited (e.g., 2 claims/year) Ideal Vehicle Age Over 5–7 years Brand new to 5 years Things to Keep in Mind The 5-Year Rule: Most insurers offer Zero Dep only for cars up to 5 years old. However, in 2026, some specialized providers extend this to 7 or even 10 years for well-maintained vehicles at a higher premium. Claim Limits: Most policies limit you to two zero-dep claims per year. Any subsequent claims in the same year will be treated as standard comprehensive claims. Exclusions: Zero Dep does not cover regular wear and tear (like tires or batteries) or mechanical breakdowns—only accidental damage. In a Nutshell Zero Depreciation insurance is the single best way to preserve the financial value of your new car. While the premium is slightly higher (roughly 15–20% more than a basic plan), the savings during a single major claim can equal several years’ worth of premiums. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Why choose zero dep Insurance for your new car Read More January 14, 2026 Precision Wealth: Why Portfolio Management Companies Are Essential Read More January 14, 2026 The Architecture of Affluence: Why Expert Wealth Management is Non-Negotiable in 2026 Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

Tips for purchasing health insurance for senior citizens

Tips for purchasing health insurance for senior citizens As we age, health becomes our greatest wealth. However, in 2026, the medical landscape has shifted: while medical inflation continues to rise at nearly 14% annually, new regulations and government schemes have made securing geriatric care more accessible than ever before. Whether you are looking for health insurance for yourself or your parents, navigating the “fine print” is essential to ensure your retirement savings remain protected. 1. Evaluate Comprehensive “Modern” Senior Plans In 2026, senior citizen plans have evolved beyond basic hospitalization. When comparing plans, prioritize these three non-negotiables: Minimal or Zero Co-payment: Historically, senior plans forced you to pay 20% of the bill out-of-pocket. Today, premium plans (like Niva Bupa ReAssure 2.0 or Star Red Carpet) offer options to waive this entirely, ensuring the insurer picks up the full tab. Shorter Waiting Periods: Traditional plans had a 4-year wait for pre-existing diseases (PED) like diabetes or hypertension. In 2026, many competitive plans have reduced this to 1–2 years, with some offering “PED Waivers” that activate coverage in just 30 days. OPD and Daycare Coverage: Many age-related treatments like dialysis, chemotherapy, and cataract surgeries no longer require a 24-hour stay. Ensure your policy covers these “Daycare” procedures and offers an OPD (Outpatient) benefit for regular consultations and diagnostics. 2. The “Ayushman Vay Vandana” Safety Net (70+ Seniors) A landmark shift in 2026 is the expansion of the Pradhan Mantri Jan Arogya Yojana (PM-JAY). Under the Ayushman Vay Vandana initiative, all senior citizens aged 70 and above are now eligible for free coverage of up to ₹5 lakh per year, regardless of income. Key Advantage: Unlike private insurance, this has zero waiting periods; pre-existing conditions are covered from Day 1. How to Apply: Seniors only need their Aadhaar card for a simple e-KYC process via the Ayushman App or a local CSC center to receive their Vay Vandana Card. 3. Individual Plans vs. Family Floaters For seniors, the “Family Floater” model—where a couple shares one pool of money—is often a trap. The Recommendation: Opt for Individual Plans. In a floater, if one spouse exhausts the limit for a major surgery, the other is left unprotected for the rest of the year. Individual plans ensure dedicated “Sum Insured” for each person. Restoration Benefit: Look for plans with “Unlimited Restoration.” If you use your ₹10 lakh limit on one illness, the policy automatically refills it for the next one, providing a infinite safety net within the same year. 4. Strategic Use of “Super Top-Ups” Buying a high-base cover (e.g., ₹25 lakh) for a senior can be prohibitively expensive. In 2026, the smart move is the Super Top-Up strategy. The Math: Buy a modest base policy of ₹5 lakh and add a ₹15 lakh Super Top-Up with a ₹5 lakh deductible. Your base policy covers the first 5 lakhs, and the Top-Up covers everything beyond that. This can reduce your premium costs by up to 30–40% while maintaining high total coverage. Critical Checklist for 2026 Buyers Feature Importance What to Look For Room Rent Critical Look for “No Room Rent Capping” to avoid pro-rata deductions. AI Claims High Choose insurers with 24-hour AI-powered cashless approvals. Annual Check-up High Essential for early detection of chronic conditions. Network Critical Ensure your preferred local multi-specialty hospital is on the “Cashless” list. In a Nutshell Securing health insurance for seniors in 2026 requires a hybrid approach: utilizing the Ayushman Vay Vandana card for a solid foundation and a Private Super Top-Up for access to premium wards and specialized doctors. By disclosing medical history accurately and prioritizing shorter waiting periods, you ensure that medical bills never compromise your peace of mind. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Elevating Your Practice: Successful Investing with a Mutual Fund Distributor Read More January 14, 2026 The Architecture of Affluence: Why Expert Wealth Management is Non-Negotiable in 2026 Read More January 14, 2026 How a financial advisor transforms your money Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

Things to keep in mind before buying car insurance

Things to keep in mind before buying car insurance In 2026, the process of buying car insurance online in India has evolved into a streamlined, tech-driven experience. However, with the rise of hyper-personalized “Pay-As-You-Drive” models and AI-powered claim settlements, making the right choice requires more than just looking for the lowest premium. Whether you are insuring a brand-new vehicle or renewing an existing policy, here are the critical factors to keep in mind to ensure your financial safety. 1. Match Coverage to Your Vehicle’s Age Choosing the right plan is the first step toward a secure drive. In the Indian market, you generally choose between: Third-Party Cover: The legal minimum mandated by the Motor Vehicles Act. It covers damages, disability, or death to others. While affordable, it offers zero protection for your own car. Comprehensive Cover: Highly recommended for new and mid-age cars. It protects against theft, fire, and natural disasters (like floods or cyclones), alongside third-party liabilities. 2. Optimize the Insured Declared Value (IDV) IDV is the maximum sum insured that the company will pay if your car is stolen or totaled. It is calculated based on the manufacturer’s listed selling price minus depreciation. The Balance: Setting a low IDV reduces your premium but can leave you with a massive financial gap in case of a total loss. Always aim for an IDV that is closest to your car’s current market value. 3. Evaluate the Claim Settlement Ratio (CSR) In 2026, an insurer’s reliability is measured by their CSR—the percentage of claims settled against those received. The Benchmark: Look for insurers with a CSR consistently above 95%. Also, check for “Self-Video Claims” or AI-based inspection features that can settle minor claims within hours rather than days. 4. Selective Use of Add-On Covers Standard policies have gaps. Customizing your plan with specific “riders” can prevent out-of-pocket expenses: Zero Depreciation: Essential for cars up to 5 years old; it ensures the insurer pays for the full cost of replaced parts without deducting for wear and tear. Engine Protection: Vital for regions prone to heavy rains, as it covers internal engine damage due to water ingression (hydrostatic lock). Return to Invoice (RTI): In the event of theft or total loss, RTI ensures you receive the original invoice value of the car, including registration and taxes. 5. Leverage the No Claim Bonus (NCB) The NCB is a reward for safe driving, offering discounts ranging from 20% to 50% on your “Own Damage” premium for every claim-free year. Pro Tip: The NCB is linked to the owner, not the car. If you sell your old car and buy a new one, you can transfer your earned NCB to the new policy to save significantly on your first premium. 6. Consider Usage-Based Insurance (UBI) A major trend in 2026 is “Pay-As-You-Drive” insurance. If you use your car primarily for short weekend trips or have a low annual mileage, these telematics-based plans can offer up to 15–20% savings compared to traditional annual policies. Summary Checklist for 2026 Feature Importance Why it Matters Cashless Garages High Minimizes upfront repair costs after an accident. Voluntary Deductible Medium Increasing this lowers premium, but increases your share of the repair cost. Digital Claims High Look for mobile-first insurers for faster processing. Network Size High Ensure your preferred service center is a “network garage.” Conclusion Buying car insurance is no longer a “one-size-fits-all” transaction. By utilizing online comparison tools and focusing on IDV accuracy and claim reliability, you can build a safety net that truly protects your mobility and your assets. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Retirement mistakes to avoid – Copy Read More January 14, 2026 PMS vs. Mutual Funds: Which One is Right for You in 2026? Read More December 30, 2025 Retirement mistakes to avoid Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch