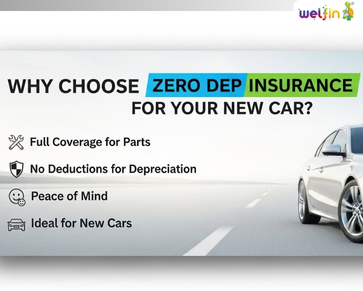

Why choose zero dep Insurance for your new car

Why choose zero dep Insurance for your new car Buying a new car is a landmark achievement. However, the moment you drive it out of the showroom, its value begins to drop due to a process called Depreciation. In 2026, where vehicle technology is more complex and repair costs are higher than ever, a standard comprehensive policy may leave you with a significant “out-of-pocket” bill after an accident. This is where Zero Depreciation (Zero Dep) insurance becomes an essential safety net. What is Zero Depreciation Insurance? Buying a new car is a landmark achievement. However, the moment you drive it out of the showroom, its value begins to drop due to a process called Depreciation. In 2026, where vehicle technology is more complex and repair costs are higher than ever, a standard comprehensive policy may leave you with a significant “out-of-pocket” bill after an accident. This is where Zero Depreciation (Zero Dep) insurance becomes an essential safety net. What is Zero Depreciation Insurance? Often called “Bumper-to-Bumper” insurance, Zero Dep is an optional add-on for your comprehensive car policy. In a standard policy, if you replace a damaged part, the insurer pays the “depreciated value” based on the part’s material and the car’s age. For example, plastic and rubber parts can see a 50% deduction. With a Zero Dep add-on, the insurer waives these deductions and pays the full cost of the parts (minus a small mandatory deductible). Why It Is Non-Negotiable for New Cars in 2026 Full Claim Payouts: Without this cover, you could end up paying for nearly half of the expensive parts (like fiber bumpers or LED headlights) out of your own pocket. High-Tech Parts Protection: Modern 2026 cars are packed with sensors and expensive electronics. Zero Dep ensures you aren’t financially burdened by the high cost of these “smart” components. Financial Predictability: It transforms an unpredictable repair bill into a fixed, manageable premium, providing peace of mind in heavy traffic. How to Check if You Have Zero Dep Policy Schedule: Look for the “Add-ons” or “Endorsements” section. It will be listed as “Nil Depreciation” or “Depreciation Reimbursement.” Premium Breakup: Check if an additional premium has been charged for this specific rider. Digital Verification: Log in to the mParivahan app or the VAHAN portal; your policy details will clearly show the “Bumper-to-Bumper” status Key Comparisons at a Glance Feature Standard Comprehensive Zero Dep Insurance Claim Settlement Based on depreciated value 100% of parts value Out-of-pocket Expense High (30% to 50% of parts) Minimal (only mandatory fees) Claim Limit Usually unlimited Often limited (e.g., 2 claims/year) Ideal Vehicle Age Over 5–7 years Brand new to 5 years Things to Keep in Mind The 5-Year Rule: Most insurers offer Zero Dep only for cars up to 5 years old. However, in 2026, some specialized providers extend this to 7 or even 10 years for well-maintained vehicles at a higher premium. Claim Limits: Most policies limit you to two zero-dep claims per year. Any subsequent claims in the same year will be treated as standard comprehensive claims. Exclusions: Zero Dep does not cover regular wear and tear (like tires or batteries) or mechanical breakdowns—only accidental damage. In a Nutshell Zero Depreciation insurance is the single best way to preserve the financial value of your new car. While the premium is slightly higher (roughly 15–20% more than a basic plan), the savings during a single major claim can equal several years’ worth of premiums. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Why choose zero dep Insurance for your new car Read More January 14, 2026 Precision Wealth: Why Portfolio Management Companies Are Essential Read More January 14, 2026 The Architecture of Affluence: Why Expert Wealth Management is Non-Negotiable in 2026 Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

Precision Wealth: Why Portfolio Management Companies Are Essential

Precision Wealth: Why Portfolio Management Companies Are Essential In the modern financial landscape, the era of “set it and forget it” investing has hit a wall. As benchmark indices hover near record highs, the market has entered what experts call the “Selectivity Shift.” This means that while the overall index might move sideways, individual sectors and stocks are showing massive divergence in performance. Navigating this “always-changing terrain” requires more than just a diversified mutual fund; it requires the methodical, surgical precision that only a Portfolio Management Company can provide. By balancing aggressive return targets with sophisticated risk-mitigation engines, these firms have become essential for anyone looking to maximize wealth in a high-volatility environment. The 2026 Regulatory Landscape: What has Changed? 1. What is Portfolio Management Today? Portfolio management is the professional “distribution center” for your wealth. It involves the choice, distribution, and constant monitoring of a varied mix of asset, including stocks, bonds, and specialized alternative investments. Unlike pooled vehicles, a PMS provider offers: Discretionary Management: Where the manager makes real-time decisions based on a pre-agreed mandate. Non-Discretionary/Advisory: Where the manager provides the research, but you maintain the final “Buy/Sell” authority. 2. Core Objectives: The “Four Pillars” of Success A Portfolio Management Company operates on four fundamental goals to ensure your capital doesn’t just grow, but survives. A. Safety and Risk Control “Risk” is no longer just market volatility. It includes Sector Rotation Risk and Policy Uncertainty. Managers use sophisticated hedging to protect your principal during extreme events, ensuring that one bad week doesn’t wipe out a year of gains. B. Strategic Return Optimization The goal is to generate “Alpha”returns that beat the standard benchmarks. In a market where corporate margins are being squeezed by new technologies, professional managers identify the winners who are leveraging innovation to stay ahead. C. Capital Preservation For investors with low risk tolerance or specific liquidity needs, managers include conservative assets like high-yield fixed income or cash equivalents. This provides a “psychological safety net” during market downturns. D. Balancing Liquidity and Time Horizons Managers ensure you have enough liquid assets to satisfy short-term cash flow needs while keeping the “Growth Engine” of the portfolio locked in for the long term. 3. The Professional Edge: Why You Need a Fund Manager If you have a corpus of ₹50 Lakh or more, managing it yourself is often a full-time job. Portfolio Management Services (PMS) offer three distinct advantages: A. Professional Expertise and “Active” Monitoring Passive investing (like Index Funds) is facing headwinds due to high concentration in a few mega-cap stocks. Fund managers provide Active Observation, rebalancing your portfolio to grab new opportunities in emerging themes like manufacturing or the AI buildout. B. Access to Exclusive Opportunities Many PMS providers offer placements or private equity deals that are simply not available to retail investors. This allows for diversification beyond traditional stocks and bonds. C. Transparency and Accountability Transparency is a core pillar of modern regulations. You receive regular, detailed reports on transaction history, expenses, and performance. This data helps you evaluate exactly how much “Alpha” your manager is adding relative to the fees paid. 4. Understanding the Cost and Taxation The cost of professional management is structured to be transparent under the new Base Expense Ratio (BER) rules. Conclusion: The New Standard for Wealth Maximizing returns is no longer about “chasing the hot trade.” It is about thoughtful position sizing and disciplined capital allocation. A Portfolio Management Company provides the institutional-grade research and execution needed to turn a collection of stocks into a resilient wealth engine. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 PMS vs. Mutual Funds: Which One is Right for You in 2026? – Duplicate – [#6495] Read More January 14, 2026 Why do you need a financial advisor for managing your funds? Read More January 14, 2026 Which health insurance is good for you Individual health insurance or a Family health Insurance plan Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

The Architecture of Affluence: Why Expert Wealth Management is Non-Negotiable in 2026

The Architecture of Affluence: Why Expert Wealth Management is Non-Negotiable in 2026 In an era defined by rapid technological shifts and a complex global economic landscape, managing significant capital has moved far beyond simple stock picking. In 2026, wealth isn’t just about what you “make”; it’s about what you keep, protect, and pass on. Think of your financial life as a high-performance aircraft. You might have the engine (your income) and the wings (your investments), but without a sophisticated navigation system and a seasoned co-pilot, you are vulnerable to the turbulence of inflation, shifting tax codes, and market unpredictability. Expert wealth management provides that navigation system, ensuring your future remains secure regardless of the “weather” outside. What Defines a Wealth Management Firm in 2026? A wealth management organization is no longer just a brokerage. It is a specialized financial architect providing a “family office” style experience. Unlike traditional advisors who may only look at your mutual fund portfolio, these firms focus on the total ecosystem of your financial life. This includes the seamless integration of: Dynamic Investment Strategies: Moving between active and passive vehicles. Tax Engineering: Real-time adjustments to new 2026 fiscal policies. Retirement & Estate Architecture: Ensuring your lifestyle remains unchanged while your legacy is codified. The Strategic Advantages of Professional Oversight The Strategic Advantages of Professional Oversight Managing your assets effectively provides more than just a higher number on a screen; it provides the psychological freedom to focus on your life, career, and family. 1. Risk Mitigation in Volatile Cycles The 2026 market has shown that “buy and hold” is often insufficient without “protect and rebalance.” Professional managers help you navigate unforeseen hazards and sector-specific swings, reducing the drawdown effect on your total net worth. 2. Radical Tax Efficiency With the current tax slabs—12.5% for Long-Term Capital Gains (LTCG) and 20% for Short-Term Capital Gains (STCG)—the “tax drag” on a portfolio can be the difference between meeting a goal and falling short. Expert wealth managers build tax-efficient exit strategies and use harvesting techniques to maximize your post-tax status. 3. Legacy and Multi-Generational Continuity Wealth is often lost in the transition between generations. Modern wealth management ensures that estate planning is not an afterthought but a core pillar. This guarantees that your fortune is handed down according to your exact preferences while minimizing the impact of estate-related levies. Why a Holistic Approach is the Only Path Forward One of the primary mistakes investors make is “compartmentalization”—treating their tax consultant, their insurance agent, and their stockbroker as separate entities. A 2026 wealth management service views your situation holistically. This “Big Picture” view allows for: Tailored Solutions: Your plan is built around your specific risk appetite and life stage, not a generic model. Access to Expertise: You gain a “Personal Board of Directors”—a team of investment managers, tax consultants, and estate planners working in sync. Long-Term Sustainability: By stressing sustainable growth over speculative gains, these services protect your capital for successive generations. Selecting Your Partner: The 2026 Criteria Selecting the right firm is the most critical investment decision you will make this year. Consider these four pillars: Experience & Reputation: Does the firm have a proven track record of protecting wealth during the market corrections of the last five years? Breadth of Service: Can they handle complex needs like international taxation or the management of unlisted shares? Transparent Fee Structures: In the wake of SEBI’s 2026 regulatory updates, ensure you understand the Base Expense Ratio (BER) and any performance-based incentives. Choose a structure that aligns their success with yours. The Relationship Quotient: Wealth management is a marathon. You need a partner who maintains open lines of communication and provides routine updates on how your roadmap is evolving. Conclusion: Securing the Horizon Ultimately, a wealth management firm acts as the guardian of your financial future. By shifting from “self-management” to “expert-led strategy,” you transition from a state of constant financial vigilance to a state of financial peace of mind. As we navigate the complexities of 2026, the question is no longer whether you can afford professional wealth management, it’s whether you can afford the cost of going without it. Protecting your family’s future requires a comprehensive plan that meets immediate needs while anchoring long-term security. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 The Architecture of Affluence: Why Expert Wealth Management is Non-Negotiable in 2026 Read More January 14, 2026 How a financial advisor transforms your money Read More January 14, 2026 Tips for purchasing health insurance for senior citizens Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

How a financial advisor transforms your money

The Coach Approach: Why Professional Financial Planning is the Key to Success in 2026 Have you ever considered why the world’s most elite athletes, individuals at the absolute pinnacle of their physical capabilities, still rely on coaches to help them perform? Even the most naturally gifted sprinter or the most strategic chess grandmaster understands that they cannot see their own blind spots. Similarly, during our formative years, instructors serve as our primary guides through education. So, why should our financial lives be any different? We need direction to succeed, to pursue our most ambitious dreams, and to grow from the inevitable mistakes we make along the way. In the modern economic landscape, financial advisors serve as our trainers, providing the same rigor and discipline found in the world of sports. They help you identify your primary objectives and then build a rigorous strategy for a successful follow-up. Defining the Modern Financial Guide Whether your current circumstances call for a holistic financial planner or a specialized investment adviser, their primary role is to help you make sense of your money by building a comprehensive financial road map. In 2026, the financial world is more complex than ever. With the integration of AI-driven markets and shifting global tax regulations, these professionals handle specific, high-stakes objectives such as: Tax Efficiency: Advanced preparation to ensure you keep more of what you earn. Retirement Engineering: Moving beyond simple savings to build a sustainable income stream. Milestone Funding: Structuring capital for property acquisitions or the rising costs of global higher education. How to Identify a Reliable Professional When seeking a guide for your wealth, look for a balance of technical prowess and human empathy. A top-tier advisor should be judged on two distinct sets of criteria: Professional Attributes: This includes certified expertise, a history of technical skill, and an uncanny ability to discern the unique needs of a consumer. Personal Traits: In an industry built on trust, you must look for honesty, patience, integrity, a genuine readiness to assist, and a level of farsightedness that looks ten to twenty years into the future. Top Strategies Financial Planning Can Provide in 2026 1. Budgeting as a Confidence Engine There is a profound psychological shift that occurs when you move from “spending what is left” to “planning what is spent.” Research in 2026 suggests that 96% of individuals with a documented financial plan are confident they will meet their long-term objectives. Furthermore, 76% of these individuals believe their economic situation is more under their control because of that plan. Financial planning lets you create a quantifiable target to aim towards. By tracking your development, you can identify and remove roadblocks before they trip you up. This level of clarity removes the ambiguity and doubt that often lead to “analysis paralysis” or emotional decision-making. 2. Overcoming the “Entry Barrier” Myth The most common excuse for lacking a financial plan is the phrase: “I don’t have enough money yet.” This is one of the most damaging myths in personal finance. Planning does not require a massive financial outlay to start. In fact, financial planning may significantly influence lower-income households more than any other group. By guiding individuals to improve their saving and budgeting practices from the ground up, a professional plan turns small, disciplined measures into significant wealth over time. A documented plan offers a means to evaluate progress and helps prioritize objectives when resources are limited. 3. Building an Integrated Investing Portfolio A professional financial plan provides you with the “whole terrain” of your life. It defines your objectives, calculates exactly how long it will take to reach them, and measures your true comfort with risk. Once you see your financial life holistically, you can work out how to achieve each personal goal through a two-pronged approach: Saving: Putting aside capital for near-term needs or emergency liquidity. Investing: Deploying money for the long run in assets that, ideally, can grow and outpace inflation. With your financial plan as a road map, you are statistically more likely to make deliberate, profitable investment choices than to go without direction and simply “hope for the best.” 4. Improving Money Habits and Quality of Life Financial planning is about far more than just “picking stocks.” It is about what money can accomplish for your confidence, security, and overall quality of life. This includes: Protection: The safety net provided by comprehensive life and health insurance. Peace of Mind: The psychological relief of having a fully-funded emergency fund. Discipline: The fostering of good financial practices that eventually become second nature. A plan transforms money from a source of stress into a tool for empowerment. 5. Customizing Planning to Your Personality No two investors are alike. Your attitude toward life affects every choice you make, including how you handle your capital. Knowing whether you are naturally risk-averse, a “spender,” or a “security seeker” helps your advisor move you in the right direction. Professional planning is not a one-size-fits-all product; it is a bespoke service tailored to fit any personality and any life stage. The Verdict for 2026 While it may seem like a hassle to sit down and map out your future, a professional financial strategy offers a basis for monitoring, understanding, and goal attainment that is impossible to achieve alone. A qualified adviser assists you in determining your true objectives and developing a strategy, whether your savings are for a specific goal like a new home or you require thorough, multi-generational asset management. Direction is the difference between wandering and arriving. In the sphere of finance, having a trainer by your side ensures that every mistake is a lesson and every success is a step toward your ultimate dream. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 How a financial advisor transforms your money Read More January 14, 2026 Is mutual fund safe – Copy Read More January 14, 2026 Things to keep in mind before buying car

Tips for purchasing health insurance for senior citizens

Tips for purchasing health insurance for senior citizens As we age, health becomes our greatest wealth. However, in 2026, the medical landscape has shifted: while medical inflation continues to rise at nearly 14% annually, new regulations and government schemes have made securing geriatric care more accessible than ever before. Whether you are looking for health insurance for yourself or your parents, navigating the “fine print” is essential to ensure your retirement savings remain protected. 1. Evaluate Comprehensive “Modern” Senior Plans In 2026, senior citizen plans have evolved beyond basic hospitalization. When comparing plans, prioritize these three non-negotiables: Minimal or Zero Co-payment: Historically, senior plans forced you to pay 20% of the bill out-of-pocket. Today, premium plans (like Niva Bupa ReAssure 2.0 or Star Red Carpet) offer options to waive this entirely, ensuring the insurer picks up the full tab. Shorter Waiting Periods: Traditional plans had a 4-year wait for pre-existing diseases (PED) like diabetes or hypertension. In 2026, many competitive plans have reduced this to 1–2 years, with some offering “PED Waivers” that activate coverage in just 30 days. OPD and Daycare Coverage: Many age-related treatments like dialysis, chemotherapy, and cataract surgeries no longer require a 24-hour stay. Ensure your policy covers these “Daycare” procedures and offers an OPD (Outpatient) benefit for regular consultations and diagnostics. 2. The “Ayushman Vay Vandana” Safety Net (70+ Seniors) A landmark shift in 2026 is the expansion of the Pradhan Mantri Jan Arogya Yojana (PM-JAY). Under the Ayushman Vay Vandana initiative, all senior citizens aged 70 and above are now eligible for free coverage of up to ₹5 lakh per year, regardless of income. Key Advantage: Unlike private insurance, this has zero waiting periods; pre-existing conditions are covered from Day 1. How to Apply: Seniors only need their Aadhaar card for a simple e-KYC process via the Ayushman App or a local CSC center to receive their Vay Vandana Card. 3. Individual Plans vs. Family Floaters For seniors, the “Family Floater” model—where a couple shares one pool of money—is often a trap. The Recommendation: Opt for Individual Plans. In a floater, if one spouse exhausts the limit for a major surgery, the other is left unprotected for the rest of the year. Individual plans ensure dedicated “Sum Insured” for each person. Restoration Benefit: Look for plans with “Unlimited Restoration.” If you use your ₹10 lakh limit on one illness, the policy automatically refills it for the next one, providing a infinite safety net within the same year. 4. Strategic Use of “Super Top-Ups” Buying a high-base cover (e.g., ₹25 lakh) for a senior can be prohibitively expensive. In 2026, the smart move is the Super Top-Up strategy. The Math: Buy a modest base policy of ₹5 lakh and add a ₹15 lakh Super Top-Up with a ₹5 lakh deductible. Your base policy covers the first 5 lakhs, and the Top-Up covers everything beyond that. This can reduce your premium costs by up to 30–40% while maintaining high total coverage. Critical Checklist for 2026 Buyers Feature Importance What to Look For Room Rent Critical Look for “No Room Rent Capping” to avoid pro-rata deductions. AI Claims High Choose insurers with 24-hour AI-powered cashless approvals. Annual Check-up High Essential for early detection of chronic conditions. Network Critical Ensure your preferred local multi-specialty hospital is on the “Cashless” list. In a Nutshell Securing health insurance for seniors in 2026 requires a hybrid approach: utilizing the Ayushman Vay Vandana card for a solid foundation and a Private Super Top-Up for access to premium wards and specialized doctors. By disclosing medical history accurately and prioritizing shorter waiting periods, you ensure that medical bills never compromise your peace of mind. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Elevating Your Practice: Successful Investing with a Mutual Fund Distributor Read More January 14, 2026 The Architecture of Affluence: Why Expert Wealth Management is Non-Negotiable in 2026 Read More January 14, 2026 How a financial advisor transforms your money Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

Things to keep in mind before buying car insurance

Things to keep in mind before buying car insurance In 2026, the process of buying car insurance online in India has evolved into a streamlined, tech-driven experience. However, with the rise of hyper-personalized “Pay-As-You-Drive” models and AI-powered claim settlements, making the right choice requires more than just looking for the lowest premium. Whether you are insuring a brand-new vehicle or renewing an existing policy, here are the critical factors to keep in mind to ensure your financial safety. 1. Match Coverage to Your Vehicle’s Age Choosing the right plan is the first step toward a secure drive. In the Indian market, you generally choose between: Third-Party Cover: The legal minimum mandated by the Motor Vehicles Act. It covers damages, disability, or death to others. While affordable, it offers zero protection for your own car. Comprehensive Cover: Highly recommended for new and mid-age cars. It protects against theft, fire, and natural disasters (like floods or cyclones), alongside third-party liabilities. 2. Optimize the Insured Declared Value (IDV) IDV is the maximum sum insured that the company will pay if your car is stolen or totaled. It is calculated based on the manufacturer’s listed selling price minus depreciation. The Balance: Setting a low IDV reduces your premium but can leave you with a massive financial gap in case of a total loss. Always aim for an IDV that is closest to your car’s current market value. 3. Evaluate the Claim Settlement Ratio (CSR) In 2026, an insurer’s reliability is measured by their CSR—the percentage of claims settled against those received. The Benchmark: Look for insurers with a CSR consistently above 95%. Also, check for “Self-Video Claims” or AI-based inspection features that can settle minor claims within hours rather than days. 4. Selective Use of Add-On Covers Standard policies have gaps. Customizing your plan with specific “riders” can prevent out-of-pocket expenses: Zero Depreciation: Essential for cars up to 5 years old; it ensures the insurer pays for the full cost of replaced parts without deducting for wear and tear. Engine Protection: Vital for regions prone to heavy rains, as it covers internal engine damage due to water ingression (hydrostatic lock). Return to Invoice (RTI): In the event of theft or total loss, RTI ensures you receive the original invoice value of the car, including registration and taxes. 5. Leverage the No Claim Bonus (NCB) The NCB is a reward for safe driving, offering discounts ranging from 20% to 50% on your “Own Damage” premium for every claim-free year. Pro Tip: The NCB is linked to the owner, not the car. If you sell your old car and buy a new one, you can transfer your earned NCB to the new policy to save significantly on your first premium. 6. Consider Usage-Based Insurance (UBI) A major trend in 2026 is “Pay-As-You-Drive” insurance. If you use your car primarily for short weekend trips or have a low annual mileage, these telematics-based plans can offer up to 15–20% savings compared to traditional annual policies. Summary Checklist for 2026 Feature Importance Why it Matters Cashless Garages High Minimizes upfront repair costs after an accident. Voluntary Deductible Medium Increasing this lowers premium, but increases your share of the repair cost. Digital Claims High Look for mobile-first insurers for faster processing. Network Size High Ensure your preferred service center is a “network garage.” Conclusion Buying car insurance is no longer a “one-size-fits-all” transaction. By utilizing online comparison tools and focusing on IDV accuracy and claim reliability, you can build a safety net that truly protects your mobility and your assets. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Retirement mistakes to avoid – Copy Read More January 14, 2026 PMS vs. Mutual Funds: Which One is Right for You in 2026? Read More December 30, 2025 Retirement mistakes to avoid Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

PMS vs. Mutual Funds: Which One is Right for You in 2026?

PMS vs. Mutual Funds: Which One is Right for You in 2026? The Indian wealth management industry has reached a historic milestone in 2026. With the SEBI (Mutual Funds) Regulations, 2026 officially replacing the decades-old 1996 framework, and the Portfolio Management Services (PMS) industry seeing record participation from the growing affluent class, investors face a more complex but rewarding set of choices. Whether you are a retail investor starting with a few thousand rupees or a High-Net-Worth Individual (HNI) managing a multi-crore corpus, choosing between a Mutual Fund (MF) and a Portfolio Management Service (PMS) is no longer just about “returns.” It is about tax efficiency, customization, and regulatory transparency. The 2026 Regulatory Landscape: What has Changed? Before diving into the comparison, it is essential to understand the structural shift that occurred this year. 1. From TER to BER (Base Expense Ratio) Starting in 2026, SEBI has unbundled mutual fund costs. The old Total Expense Ratio (TER) has been replaced by the Base Expense Ratio (BER). Under this new “What You See is What You Pay” model, statutory levies like GST and STT are charged on actuals rather than being hidden inside a flat percentage. This has significantly improved cost transparency for MF investors. 2. New Capital Gains Tax Slabs Following the 2024 budget reforms, the tax landscape for both products has settled: Long-Term Capital Gains (LTCG): 12.5% (for holdings over 1 year, with an exemption limit of ₹1.25 lakh). Short-Term Capital Gains (STCG): 20%. What are Mutual Funds in 2026? Mutual Funds remain the most democratic investment vehicle in India. They pool money from millions of investors to invest in a diversified basket of equities, debt, or hybrid assets. The 2026 Advantage: The rise of Passive Investing and Smart-Beta ETFs has made mutual funds incredibly cost-effective. For a “core” portfolio, mutual funds offer unmatched liquidity and safety, overseen by the most stringent regulatory framework in the world. What is a Portfolio Management Service (PMS)? PMS is a premium investment platform where a professional manager builds a customized portfolio of stocks for you. Unlike a mutual fund, where you own “units,” in a PMS, you hold the direct ownership of stocks in your own Demat account. The 2026 Advantage: In a market where large-cap stocks are efficiently priced, PMS managers provide “Alpha” (excess returns) by taking concentrated bets on mid-cap and small-cap sectors that are too small for large mutual funds to enter. PMS vs. Mutual Funds: A 1,000-Foot Comparison Feature Mutual Funds (MF) Portfolio Management (PMS) Minimum Ticket Size ₹100 – ₹500 (via SIP) ₹50 Lakhs (SEBI Mandated) Account Structure Pooled Account Individual Demat Account Customization Zero (Standardized for all) High (Bespoke strategies) Fee Model Base Expense Ratio (BER) Fixed Fee + Performance Fee Tax Trigger Only upon redemption of units On every trade made by manager Transparency High (Monthly disclosures) Real-time (Direct Demat view) 5 Critical Factors to Consider Before Investing 1. Cost Efficiency vs. Performance Incentives In 2026, the Mutual Fund BER for most equity funds hovers between 0.90% and 1.80%. It is an “all-weather” low-cost model.PMS fees, however, are aggressive. Most providers charge a 2% fixed fee and a 20% performance fee over a “hurdle rate” (usually 10-12% returns). For a PMS to be worth it, the manager must consistently beat the index by at least 3-4% to cover the extra costs. 2. The “Taxation Drag” in PMS This is where many investors are caught off guard. In a Mutual Fund, the fund manager can churn the portfolio 100 times a year, and you pay zero tax until you sell your units. In a PMS, you are the owner of the stocks. If the manager sells a stock to book profit, it triggers a tax liability for you in that financial year. For high-churn strategies, this “tax drag” can eat into your net returns. 3. Concentration Risk vs. Diversification Mutual funds are legally barred from investing more than 10% in a single stock. This protects you from a single company’s collapse. PMS managers often run “High Conviction” portfolios with just 15-20 stocks. While this leads to massive outperformance during bull runs, it can result in deeper drawdowns during market corrections. 4. Customization and Exclusion If you are an executive in a major bank, you might already have enough exposure to BFSI. 5. Transparency and Control With the digital integration of 2026, PMS investors can see every trade on their mobile apps the moment it happens. You can see exactly what price the manager bought a stock for. Mutual funds provide a “Factsheet” every month, which is a snapshot, not a real-time movie of the fund’s activity. Who Should Choose What? Choose Mutual Funds if: You are building wealth systematically through SIPs. Your investible surplus is below ₹50 Lakhs. You prefer a “set it and forget it” approach with high liquidity. You want to take advantage of the tax-free internal compounding of a fund. Choose PMS if: You have a portfolio of ₹1 Crore+ and want personalized attention. You are seeking Alpha in mid-cap/small-cap spaces that mutual funds can’t touch due to size constraints. You want Direct Ownership and the ability to track every individual trade. You have a high risk-appetite and can handle the volatility of a concentrated portfolio. Conclusion The choice between PMS and Mutual Funds in 2026 isn’t about which is “better”, it’s about which serves your current financial stage. Mutual Funds are the most efficient vehicle for wealth preservation and steady growth, while PMS is a powerful tool for aggressive wealth acceleration for the sophisticated investor. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” January 14, 2026 Is mutual fund safe – Copy Read More January 14, 2026 Things to keep in mind before buying car insurance Read More January 14, 2026 PMS vs. Mutual Funds: Which One is Right for You in 2026? Read More Confused about money decisions? Get clarity on investments, insurance & goals in one

Retirement mistakes to avoid

Retirement Mistakes to Avoid Retirement is often viewed as a time to relax and enjoy the rewards of decades of hard work. However, for many people, retirement brings financial stress rather than comfort, not because they did not earn enough, but because they made avoidable planning mistakes. Understanding retirement mistakes to avoid is crucial for building a secure and independent post-retirement life. Retirement planning is not just about saving money. It involves managing expenses, preparing for healthcare costs, adjusting investments over time, and making realistic assumptions about the future. Small mistakes made today can have a significant impact on financial stability later. This blog explores the most common retirement mistakes and explains how avoiding them can help ensure a more confident and stress-free retirement. 1. Starting Retirement Planning Too Late One of the biggest retirement mistakes to avoid is delaying the planning process. Many people believe they have plenty of time and postpone saving for retirement until their 40s or 50s. Starting late means: Less time for compounding to work Higher monthly savings required Increased financial pressure closer to retirement 2. Underestimating Life Expectancy People often plan their retirement finances assuming they will live only a few years after retirement. However, with improved healthcare and lifestyle changes, many individuals live well into their 80s or even 90s. Underestimating life expectancy can result in: Running out of savings Reduced quality of life in later years Dependence on family members 3. Ignoring Inflation Inflation is a silent threat that can significantly reduce the purchasing power of your money over time. One of the most common retirement mistakes to avoid is planning expenses based on today’s costs without adjusting for future inflation. Even moderate inflation can double living expenses over a long retirement period. Ignoring this factor can lead to insufficient savings and unexpected financial stress. 4. Not Planning for Healthcare Expenses Healthcare costs tend to increase with age, making medical expenses one of the biggest financial risks during retirement. Many people underestimate how much they will need for medical care and long-term treatment. Failing to plan for healthcare can result in: Using retirement savings for medical emergencies Compromising on quality treatment Financial dependence during old age 5. Relying Only on Fixed Income Sources While fixed income investments offer stability, relying entirely on them can be risky. Fixed returns may not keep up with inflation, especially during long retirement periods. A common retirement mistake is avoiding growth-oriented investments altogether. A balanced approach that includes some growth assets can help maintain purchasing power while managing risk. 6. Not Diversifying Investments Putting all retirement savings into a single investment or asset class increases risk. Lack of diversification makes your retirement corpus vulnerable to market fluctuations or economic changes. Diversifying investments across different asset classes helps: Reduce overall risk Provide stable returns Protect against unexpected losses 7. Withdrawing Retirement Savings Too Early Early withdrawals from retirement savings can significantly impact long-term financial security. Withdrawing funds before retirement not only reduces the corpus but also limits the power of compounding. Using retirement funds for short-term needs is a retirement mistake that can be difficult to recover from later. 8. Overestimating Post-Retirement Income Many people assume they will continue earning through part-time work, business income, or rentals after retirement. While this may happen for some, relying too heavily on uncertain income sources can be risky. Retirement plans should be built on realistic assumptions rather than optimistic expectations. 9. Failing to Review and Update Retirement Plans Life changes over time, and retirement plans must adapt accordingly. One of the most overlooked retirement mistakes to avoid is failing to review plans regularly. Major life events such as: Marriage or family changes Career shifts Health issues Economic changes 10. Not Having an Emergency Fund Many retirees face unexpected expenses such as medical emergencies, home repairs, or family responsibilities. Without an emergency fund, these expenses may force retirees to dip into long-term savings. An emergency fund acts as a financial buffer and helps protect retirement investments from premature withdrawals. Final Thoughts: Avoid Mistakes, Secure Your Retirement Retirement planning is a long-term process that requires foresight, discipline, and regular review. Understanding retirement mistakes to avoid can help individuals make smarter decisions and protect their financial future. By starting early, planning realistically, diversifying investments, and preparing for healthcare and inflation, retirees can enjoy financial stability and peace of mind. Avoiding common mistakes today can make the difference between a stressful retirement and a comfortable, independent one. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” December 30, 2025 retirement mistakes to avoid Read More December 30, 2025 Is mutual fund safe Read More December 30, 2025 difference between sip and mutual fund Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

Is mutual fund safe

Is Mutual Fund Safe? A Clear and Honest Guide for Investors One of the most common questions asked by people who are new to investing is: Is mutual fund safe? The concern is understandable. Investing involves risk, and with market fluctuations, economic uncertainty, and news about financial losses, investors want reassurance before putting their hard-earned money into mutual funds. The short answer is: Mutual funds are generally safe when chosen wisely, but they are not risk-free.This blog explains what “safety” really means in mutual funds, the risks involved, how mutual funds are regulated, and how investors can reduce risk while investing. What Does “Safe” Mean in Investing? Before deciding whether mutual funds are safe, it is important to understand what safety means in the context of investments. In finance, safety does not mean guaranteed returns. Instead, it refers to: Protection from fraud Transparency in operations Regulation by authorities Risk spread across multiple assets Suitability for long-term wealth creation What Is a Mutual Fund? A mutual fund is an investment vehicle that collects money from multiple investors and invests it in a diversified portfolio of assets such as stocks, bonds, or money market instruments. These funds are managed by professional fund managers who follow a defined investment strategy. Investors own units of the mutual fund, and the value of these units changes daily based on the performance of the underlying assets. Every year you delay, your future self pays. A ₹10,000 monthly SIP started today for 20 years can grow to a far larger corpus than the same SIP started 5 years later. Waiting costs you lakhs in lost compounding. Monthly SIP Amount ₹10,000 Expected Annual Return 12% Investment Duration 20 yrs Returns shown are indicative and for illustration only. Get my free plan in 24 hours Investment Breakdown Invested Amount Estimated Returns Estimated Value at Maturity ₹0 Are Mutual Funds Safe From Fraud? Yes, mutual funds are considered safe from fraud because they are tightly regulated. In India, mutual funds are regulated by SEBI (Securities and Exchange Board of India). SEBI enforces strict rules regarding: Fund management Disclosure of portfolio holdings NAV calculation Investor protection Audits and compliance Types of Risks in Mutual Funds To understand whether mutual funds are safe, it is essential to understand the risks involved. Market Risk: Equity mutual funds are affected by stock market movements. Short-term volatility can cause temporary losses, especially during market downturns. Credit Risk: Debt mutual funds may face risk if the issuer of a bond defaults on payments. Interest Rate Risk Changes in interest rates can impact the value of debt funds. Inflation Risk: If returns do not beat inflation, the real value of money may reduce over time. Are All Mutual Funds Equally Safe? No. Safety depends on the type of mutual fund. Equity Mutual Funds Higher risk in the short term Suitable for long-term investors Potential for higher returns Not ideal for short-term safety Debt Mutual Funds Lower risk compared to equity funds More stable returns Suitable for conservative investors Hybrid Mutual Funds Balance between risk and stability Combine equity and debt investments Liquid and Money Market Funds Considered among the safest mutual fund categories Low volatility Suitable for short-term parking of funds How Diversification Improves Mutual Fund Safety One of the biggest advantages of mutual funds is diversification. Instead of investing in one company or bond, a mutual fund spreads investments across multiple securities. This reduces the impact of poor performance by any single asset. Diversification helps: Lower overall risk Reduce volatility Protect investors from major losses Is SIP Safer Than Lump Sum Investment? Many investors use SIP (Systematic Investment Plan) to reduce risk. SIP does not remove market risk, but it helps manage it by: Spreading investments over time Reducing the impact of market timing Encouraging disciplined investing Are Mutual Funds Safe for Beginners? Yes, mutual funds are considered one of the safest entry points for beginners, provided: The right fund type is chosen Investments match financial goals Risk tolerance is understood Beginners often benefit from: Professional fund management Small minimum investment amounts Transparent performance tracking Easy liquidity Can You Lose Money in Mutual Funds? Yes, it is possible to lose money in mutual funds, especially in the short term. However: Losses are usually temporary for long-term investors Risk reduces with time and diversification Proper fund selection significantly lowers risk Mutual funds are not gambling instruments, they are structured investment tools designed for long-term wealth creation. Final Verdict: Is Mutual Fund Safe? So, is mutual fund safe? The honest answer is: Yes, mutual funds are safe when used correctly, but they are not risk-free. They are regulated, transparent, diversified, and professionally managed, making them one of the most reliable investment options available today. While short-term fluctuations are unavoidable, long-term investors who choose suitable funds and stay invested are generally well rewarded. Mutual funds are not about eliminating risk, they are about managing risk smartly. WELFIN INSIGHT “The right insurance amount is not the cheapest or the highest it’s the one that fits your life.” December 30, 2025 retirement mistakes to avoid Read More December 30, 2025 Is mutual fund safe Read More December 30, 2025 difference between sip and mutual fund Read More Confused about money decisions? Get clarity on investments, insurance & goals in one plan. Check Now Not sure if your insurance is enough? 👉 Get a Free Insurance Adequacy Check Get In Touch

Difference between sip and mutual fund

Difference Between SIP and Mutual Fund: A Complete Guide for Smart Investors When people begin their investment journey, two terms frequently come up, SIP and mutual fund. These terms are often used interchangeably, which creates confusion, especially among new investors. Many believe SIP and mutual funds are two different investment products, while others assume they are the same thing. In reality, SIP and mutual funds are closely related but serve different purposes. Understanding the difference between SIP and mutual fund is essential for making informed investment decisions, setting realistic financial goals, and choosing the right strategy for long-term wealth creation. This blog explains the concepts in simple terms, compares SIP and mutual funds across key parameters, and helps you understand how both work together. What Is a Mutual Fund? A mutual fund is an investment vehicle that pools money from multiple investors and invests it in a diversified portfolio of assets such as equities (stocks), debt instruments (bonds), or a combination of both. These funds are managed by professional fund managers who make investment decisions based on the fund’s objective. Each investor owns units of the mutual fund proportional to the amount invested. The value of these units changes daily based on the performance of the underlying assets, known as the Net Asset Value (NAV). Key Features of Mutual Funds Professionally managed investments Diversification across multiple securities Suitable for different risk profiles Options available for short-term and long-term goals Regulated by financial authorities Types of Mutual Funds Mutual funds are categorized based on their investment objective and asset allocation: Equity Mutual Funds: Invest primarily in stocks and aim for higher long-term returns. Suitable for investors with higher risk tolerance. Debt Mutual Funds: Invest in fixed-income instruments like bonds and government securities. They offer relatively stable returns with lower risk. Hybrid Mutual Funds: Combine equity and debt investments to balance risk and return. Index Funds: Track a specific market index and aim to replicate its performance. Liquid and Money Market Funds: Focus on short-term instruments and are suitable for parking surplus funds. What Is SIP? A Systematic Investment Plan (SIP) is not an investment product but a method of investing in mutual funds. SIP allows investors to invest a fixed amount of money at regular intervals, monthly, quarterly, or weekly, into a chosen mutual fund scheme. Instead of investing a large sum at once, SIP encourages disciplined investing by spreading investments over time. This approach helps investors build wealth gradually and reduces the impact of market volatility. Key Features of SIP: Fixed investment amount at regular intervals Promotes financial discipline Reduces timing-related market risk Suitable for salaried and long-term investors Flexible, can be started, paused, or modified How SIP Works in Mutual Funds When you invest through SIP, a fixed amount is automatically invested in a mutual fund on a predetermined date. Depending on the NAV on that day, you receive a certain number of units. When markets are high, you receive fewer units. When markets are low, you receive more units. Over time, this results in rupee cost averaging, which helps lower the average cost of investment. SIP works best for long-term investments where market fluctuations are smoothed out over time. Difference Between SIP and Mutual Fund Understanding the difference between SIP and mutual fund becomes easier when you realize that a mutual fund is the investment, while SIP is one way of investing in it. Nature: A mutual fund is a financial product. SIP is an investment method used to invest in mutual funds. Investment Approach: Mutual funds allow both lump-sum and SIP investments. SIP involves periodic, fixed investments instead of a one-time investment. Flexibility: Mutual funds offer various schemes with different objectives. SIP offers flexibility in investment amount, frequency, and duration. Risk Management: Mutual funds carry market-related risks depending on the asset class. SIP helps manage market volatility by spreading investments over time. Suitability: Mutual funds are suitable for all types of investors depending on the scheme. SIP is especially suitable for beginners and salaried individuals. Investment Discipline: Mutual funds do not enforce discipline by themselves. SIP promotes disciplined and regular investing. SIP vs Lump Sum Investment in Mutual Funds One common confusion is choosing between SIP and lump-sum investment. SIP Investment: Ideal for long-term goals Reduces impact of market timing Lower initial investment requirement Encourages consistent investing Lump-Sum Investment: Suitable when markets are undervalued Requires significant capital upfront Higher exposure to market timing risk Both methods have their place, but SIP is often preferred for long-term retail investors due to its simplicity and consistency. Benefits of SIP in Mutual Funds SIP has gained popularity because of the advantages it offers: Rupee Cost Averaging: By investing regularly, investors buy more units when prices are low and fewer when prices are high. Power of Compounding: Long-term SIP investments benefit significantly from compounding, where returns generate further returns. Affordability: SIPs can be started with small amounts, making mutual fund investing accessible to a wider audience. Emotional Control: SIP reduces emotional decision-making during market highs and lows. Benefits of Mutual Funds as an Investment Mutual funds offer advantages beyond SIP: Professional fund management Diversification across assets Transparency and regulation Wide range of options for different goals Liquidity and ease of redemption Whether invested via SIP or lump sum, mutual funds remain one of the most popular investment options for long-term wealth creation. Common Misconceptions About SIP and Mutual Funds Many investors believe SIP and mutual funds are separate investment products. In reality, SIP is simply a route to invest in mutual funds. Another misconception is that SIP guarantees returns. SIP does not eliminate market risk—it only helps manage volatility over time. Some also assume SIP is only for small investors. In fact, even high-net-worth individuals use SIPs for disciplined investing. Which Is Better: SIP or Mutual Fund? This is not the right question to ask, because SIP and mutual funds are not alternatives. The correct approach is to decide: Which mutual fund suits your goal and risk profile Whether SIP